GETTING YOUR HOME LOAN

SHOULDN'T BE COMPLICATED

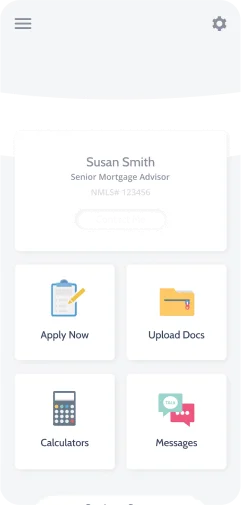

Our system guides you through the application process and connects you directly to your loan officer and realtor.

In Loans Funded

Customer Satisfaction Rate

Average Loan Approval Period

Welcome to LENDING CORNER

The Lending Corner Team is composed of true mortgage professionals that offer the lowest mortgage rates in the market today. All of our originators are principals in the company carrying over 20 years experience and work together to provide you a level of service and professionalism unparalleled in the industry.

Whether you are financing a new home purchase or refinancing an existing loan, Lending Corner has embraced all aspects of technology available to create a completely paperless and seamless transaction for our clients. Come get the service and rates you deserve with Lending Corner.

Our system guides you through the application process and connects you directly to your loan officer and realtor.

Calculate how much your monthly mortgage payment could be.

* Results are hypothetical and may not be accurate. This is not a commitment to lend nor a preapproval. Consult a financial professional for full details.

See All Mortgage Calculators